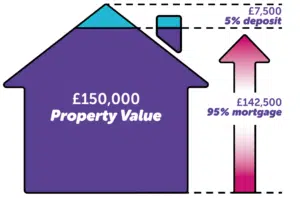

As the name would suggest, a 95% mortgage is where you are borrowing against 95% of the property price, paying the remaining 5% with your deposit. An example of this would be if you wanted to buy a property that was worth £150,000 with a 95% mortgage, your minimum deposit would be £7,500 and you would borrow the remaining £142,500 from the lender.

95% Mortgage Advice in Liverpool

Following on from the March 2021 Budget, Prime Minister Boris Johnson announced a Mortgage Guarantee Scheme for mortgage lenders, something that would aim to make 95% mortgages more readily available from the high street banks.

This is very welcome news for First-Time Buyers and Home Movers, as this scheme will remain active until December 2022. Specific terms and conditions will apply, something your Mortgage Advisor in Liverpool will be able to look at with you, to see if you qualify.

All our customers who Get in Touch with us for Mortgage Advice in Liverpool, will receive a free, no-obligation mortgage consultation. Here, one of our dedicated mortgage advisors will be able to make a recommendation on the most appropriate route for you to take.

Can I get a 95% mortgage?

You will find that 95% mortgages are usually accessible by both First-Time Buyers in Liverpool & those who are Moving Home in Liverpool. The concept of saving for a 5% deposit sounds like a pretty straightforward plan of action, but you’ll still need to have an acceptable credit score and prove to the lender that you are able to afford your monthly mortgage repayments, before you are considered for a 95% mortgage.

Improving your credit score

You’ll need to demonstrate you have a good credit score before you’ll be accepted for any mortgage, especially a 95% mortgage. Handy tips for improving this will include paying any current credit commitments on time, ensuring your addresses are updated and checking that you’re on the voters roll. For a more detailed look at how and why you can help your credit score, please see our How to Improve Your Credit Score article.

Affordability

Affordability is something else you should also consider. Providing the lender with enough details of your income and monthly outgoings (things like your bank statements will be necessary for this) and any pre-existing credit commitments will allow them to get a general overview of whether or not you are able to afford a 95% mortgage.

Can my family help me get a 95% mortgage?

It’s a common occurrence these days to see lots of family members helping one another get onto the property ladder, especially with parents looking to further their children’s lives. This normally happens by a family member gifting the person looking to find their home, the deposit required to proceed. Known through the industry as the “Bank of Mum & Dad, Gifted Deposits should only be a gift, and not a loan to be paid back. The lender will need this to be agreed and proven, before it can be used towards your mortgage.

How do I choose the right 95% mortgage?

You always want to make sure you have the right type of mortgage, especially with something like a 95% mortgage. Each type works in its own way, with that choice allowing you to find one that is most appropriate for your personal and financial circumstances.

Some homeowners and buyers would rather go with a Fixed Rate or Tracker Mortgage, mortgage types which mean you either keep interest rates at a set amount or have your interest rates following the Bank of England base rates.

Alternatively, you might be more comfortable with the way Interest-Only or a Repayment Mortgages work. Interest-Only allows cheaper payments until you need to pay a lump sum once it reaches its end (mostly now used for Buy-to-Lets), whereas a Repayment mortgage (a normal mortgage if you’d like) means you’ll be paying a combination of both interest and capital per month.

You can read more about each of these mortgage types in our Different Types of Mortgages article, with informative videos for each type.

How can a bigger deposit help with my mortgage?

A mortgage is a hugely important financial outgoing, and as such you need to be prepared. If you aren’t prepared, you might find yourself more likely to be affected by things like higher interest rates, remortgaging difficulties due to less equity and then negative equity.

This is not something to worry about though, as these problems can be avoided if you’re smart enough with your process initially. The more deposit you put down, the less risk you’ll be to the lender.

A larger deposit would not only reduce the interest rates by a noticeable amount, but would also give the property more equity and reduce the risk of negative equity, which will be because you are borrowing less against the property.

So, whilst the risks may seem rather scary at first, planning ahead and saving for a larger deposit to access something like a 90% or even an 85% mortgage will be very beneficial in your mortgage journey and something you’ll be able to reap the rewards from in the future.

Date Last Edited: August 7, 2023